By: Diane Darling

An Evil Stepmother’s Guide for Teaching Your Child Personal Finance, PART 3

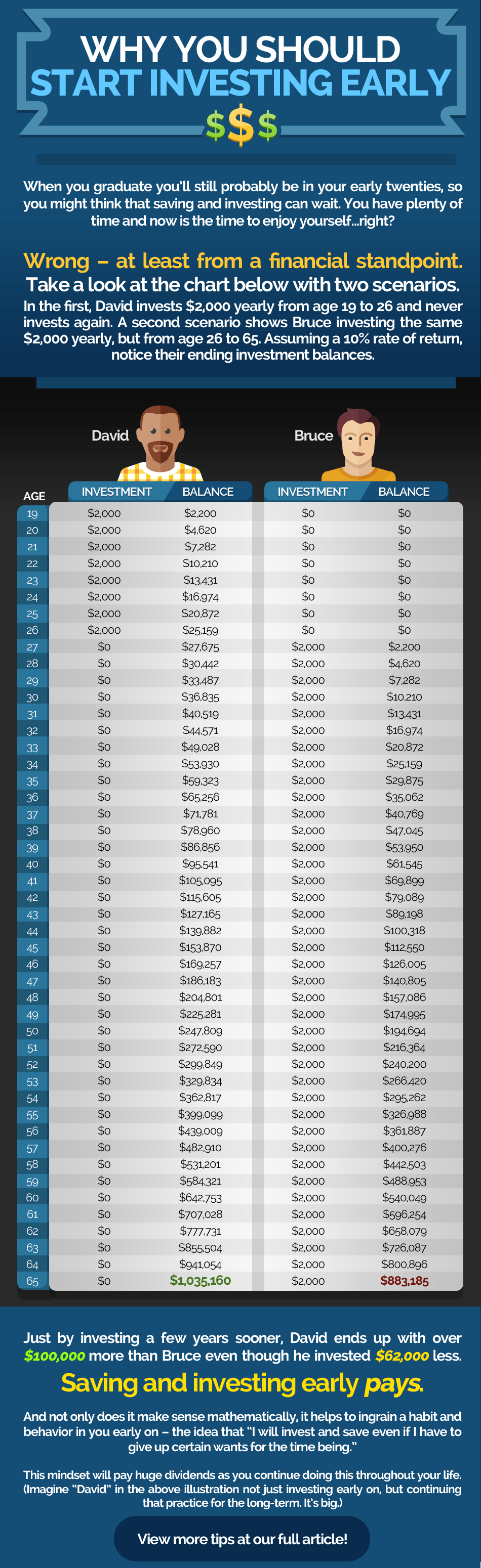

In Part 1 of this series, we explored about how to talk to your kids about their money. In Part 2, we discussed how your children might earn money with which to learn financial literacy. In this part of the series, we’ll have some actionable items about how to help your kids learn about long term saving and investing – something my partner and I didn’t learn until ages 33 and 25, respectively! Setting your kids up with this knowledge early will absolutely benefit them in the long run.

Here are some tips for thinking like an Evil Stepmother with your kids in regard to learning about delayed gratification in investing, the value of compound interest, and best practices for relatives’ generosity:

- Teaching about the market. Instead of presents (or too many presents, if you’re kinder than an Evil Stepmother), consider cutting back and giving money for the express purpose of investing. Allow your preteen/teen child to research and choose the stocks he or she would like to buy – Nike, Playstation, and Youtube might be of interest! As an Evil Stepmother, I no longer buy my stepson birthday or holiday presents, but instead invest for him using this method (with his input) in an account in my name, the money in which I plan to give to him when he turns 18.

*Though I have not used these so I cannot professionally recommend them, options for doing this might be through companies like Robinhood, Acorns, or Ellevest.*

**It is important to note that this is a learning tool for your child, not a recommendation for you as an adult – please remember that it is not recommended that you buy individual stocks as a primary means of saving for retirement!**

- Money for investing in your child’s future. Grandparents/aunts/uncles/stepparents/ other well-meaning relatives often want to know how to help contribute to your child’s future, and this can be a stress-inducing and confusing question. There are traditionally four options for this.

-

- You can recommend that they contribute to your child’s 529 Plan, or “Qualified Tuition Plan.” Keep in mind that should your child turn out to not be the college-going type, they can still use this money for other educational purposes; they might, however, be penalized for withdrawing money for other reasons (first car, first house, year abroad, etc).

- Another option for relatives might be to start an investment account in their own name with the goal of giving the money to the child when the child turns 18. This is a great investment option for relatives, as the money is still technically in the relative’s control just in case their financial situation changes unexpectedly.

- Depending on your child’s age and work situation, there are two more options that might be a good fit for relatives who want to give money to your child. You should consider tax implications and fees for both options before making a decision. You could consider starting a Custodial Brokerage Account; this is an account started on behalf of a minor child for the express purpose of earning for the child.

- The last type of account is something that might sound familiar – a Roth IRA. If your child is old enough to work (or, by IRS definition, has “earned income”), you can also start a Roth IRA for them – as we know, the sooner someone starts saving for retirement the better! Please note that the stipulations for starting a Roth IRA for your child are specific and should be examined carefully before going this route.

As your children get older and learn more about money, your approach in teaching them financial responsibility may change – but throughout their childhood, teaching them the Evil Stepmother values of saving long-term, working hard, and being generous will set them up for a strong financial future.

{kind=link}