22% of women aren’t involved in their own retirement planning. Can you believe that?

(Source included below).

While we’ve made leaps and bounds of progress in the recent decades to find more financial equality in the household, we still aren’t there, and this number illustrates a larger problem at hand. Women still don’t have an equal seat at the table. What can we do to change this?

-

- Financial Education – across the board. Why are we leaving anybody out of this conversation?

- Do away with the notion that personal finance is “taboo”, or “tacky”. Knowledge is power.

- Advocate for yourself and others.

Being actively involved in the planning and execution of your financial goals has a tremendous impact on your outcomes. When women are left out of the conversation, this opens up opportunities for financial infidelity, lack of understanding in how to manage personal finances, and a lack of awareness for what retirement will look like. Actively participating can ensure that you have retirement accounts in your name, and that you know you’re taken care of in your old age (regardless of if your marriage works out).

One of the most common ways that women get the short-end of the stick is by most often being the ones caring for their children at home (especially during their younger years). While they may not be actively bringing in money, they are saving the family significant dough by doing it. Also, it is not rainbows and butterflies. Attentive parenting takes hard work, and many stay-at-home parents would agree – going to work sounds like a bit of a vacation from the mental/emotional challenge of raising a toddler. Just because one parent is staying home, doesn’t mean their retirement contributions should suffer (regardless of which parent is doing so). They still deserve equivalent contributions if it was a joint decision for the overall benefit of the family unit that they stay home to raise children. The best way to navigate this discussion is to communicate openly and honestly. Does one of you have higher earning potential? Does one of you enjoy working more than the other? Is it worth it financially to have both parents go to work if you need to put 2 children in daycare for $1500-$1800/month? In some cases, the answer might be yes! But it depends on a lot of factors. And only you know the details of your situation and what will be best for your family.

I’ll send you off with this:

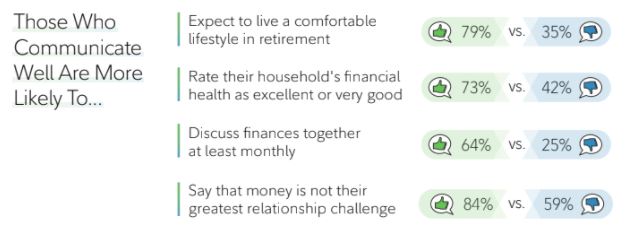

Fidelity conducted a study in 2021 on Couples & Money. One key finding was how important communication was. It’s one of the biggest indicators of financial success and relational well-being (see image below). There are a lot of interesting findings in their study, so do yourself a favor and check it out!

*Those who say they communicate well vs. those who do not.