By: Laura Walton AFC®

A new investor’s first mutual fund purchase is often a target-date fund. Why is that?

A little history. Target-date funds were first offered in 1994 but, according to Brightscope, didn’t gain traction until the Pension Protection Act of 2006. That Act required 401k’s to offer better default investment options. Until then if an employee didn’t select an investment their 401k contribution was put into a low risk, low return money market fund.

Today about 70% of U.S. companies automatically enroll their employees into their 401k plan and 86% of these firms direct the employee’s investment to their age appropriate target-date fund if no other choice is selected. According to a recent discussion on Marketplace, this has improved participants’ retirement security by 50% over a 30 year period by simply improving their returns.

Today 9 out of 10 plan sponsors offer target-date funds and Fidelity reports that 68% of millennials have 100% of their assets invested in a target-date fund.

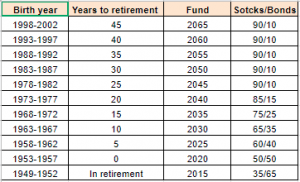

Target-date funds (also called life-cycle or target-retirement) are offered in 5-year increments ranging from 2015 to 2065. The investor simply picks the date that most closely matches his planned retirement allowing him to “set it and forget it”. The funds are structured to follow a glidepath to retirement – higher risk (more stocks) for a distant retirement date changing to lower risk (more bonds) as retirement looms.

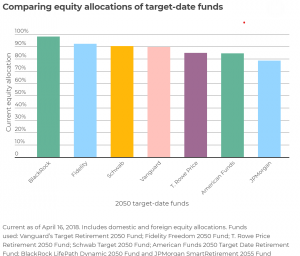

But, all target-date funds aren’t created equal. Fees average .73% and can exceed 1% (Vanguard’s range from .13-.15%). And their glidepaths can differ. “To” funds reach the target date with a low risk allocation and hold it while “through” funds hold more stock at retirement to improve returns over a longer period.

Target-date funds help us be better investors: by simply picking our retirement date, they decide on an appropriate asset allocation for us and, more importantly, they automatically and continuously rebalance that allocation for us, a task individual investors often overlook.

Most would agree that target-date funds have simplified investing resulting in improved outcomes for investors – a new and improved product we can all appreciate.